In recent years it has become clear that the technology sector has been an important driver of market growth. Innovations, especially in generative AI, are rapidly improving software capabilities, creating the potential for greater productivity and adaptability in digital tools.

But while software plays a crucial role, these advances couldn’t happen without the hardware that powers them. This underlines attractive investment opportunities in technology companies that provide the server hardware needed to run AI applications.

In this context, Vijay Rakesh, a five-star analyst at Mizuho, has shifted his focus to the AI space, specifically targeting server hardware.

“Generative AI is driving growth and disruption across multiple markets, pushing the boundaries of innovation and productivity. AI servers are the infrastructure that enables the AI revolution,” Rakesh opined. “The AI server market is expected to be ~$406 billion by 2027, with a CAGR of ~54%, driven by CSPs (Hyperscale and Tier 2) and enterprise demand. We see GenAI growing exponentially and supporting secular growth in the AI server market.”

However, not all AI stocks are created equal, and some offer better investment prospects than others. Rakesh highlights two key players in this space, Super Micro Computer (NASDAQ:SMCI) and Dell Technologies (NYSE:DELL), and offers insight into which AI stocks stand out as a must-buy stock. Let’s dive into both, using the latest data from TipRanks alongside insights from Mizuho’s report.

Super microcomputer

We start with a look at Super Micro Computer, a Silicon Valley high-tech company that specializes in developing and manufacturing the hardware behind high-performance computing and high-end server stacks. In addition, Super Micro provides management software and memory storage systems for a wide range of enterprise-level applications, including AI, cloud computing, data centers, edge computing and 5G networks.

This company has been around for over thirty years and has established itself as the go-to provider for advanced computing needs. Super Micro has the expertise to design and build complex server stacks and powerful computers and can install these systems at any scale. The company has product lines available for customization, to meet customers’ idiosyncratic needs, or off-the-shelf products, and can even handle unique or unusual design requests. Super Micro supports its product offering with a large-scale manufacturing footprint and can produce approximately 5,000 AI, HPC and liquid cooling rack solutions every month.

From a customer perspective, especially those AI customers, the key point here is the ability of Super Micro’s products – the servers, the powerful computers, the advanced memory storage – to meet the needs of the contemporary advanced technology. .

On the financial side, Super Micro generated $5.3 billion in revenue in its last reported quarter, the fiscal fourth quarter of ’24. This was an impressive 143% increase over the same period last year, exceeding forecast by $10 million. However, the company’s fourth-quarter earnings per share of $6.25 by non-GAAP measures was $1.56 per share below estimates. The company attributed the miss to a combination of lower gross margins and higher operating costs in the quarter.

We should note here that SMCI shares have fallen sharply from their recent peak, which was reached in March this year. Since then, not helped by a scathing short seller report and a 10K filing delay, the stock has fallen 61%, though it’s still up about 63% this year. Meanwhile, the company’s management has approved a 10-for-1 stock split, effective October 1 this year.

For Mizuho’s Rakesh, the key point here is that the AI hardware segment is becoming increasingly crowded and Super Micro is facing increasing competition, resulting in a loss of market share. He writes about the company: “We recognize SMCI as a consensus AI leader (AI Server ~70% of revenue), but increasing competition, market share loss (SMCI market share in AI servers down from ~80-100% by 2022 -2023). to 40-50% by 2024E), and continued competition from DELL and other competitors is putting pressure on prices and margins. We estimate that the current delays of 10,000 shares represent a headwind of approximately 10%, and we do not foresee any delisting of shares as the delays relate to internal process controls. We still view share loss and margin pressure as important valuation drivers and justify a 17% discount to the historical average ~12x.”

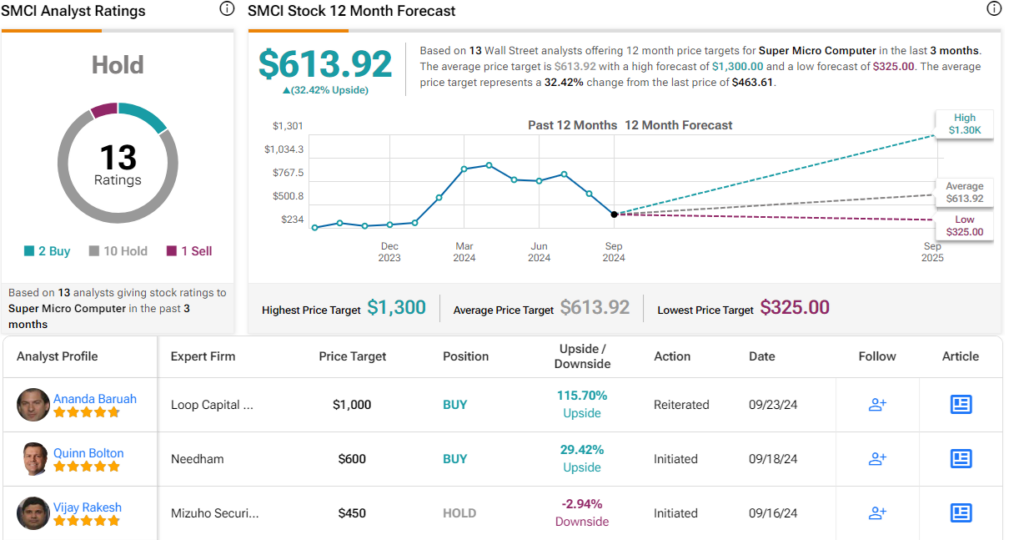

Rakesh follows up these comments with a Neutral (Hold) rating on the stock, along with a $450 price target that suggests the stock will remain relatively flat over the next year. (To view Rakesh’s track record, click here)

Overall, SMCI gets a Hold consensus from the Street, based on 13 ratings, including 2 Buys, 10 Holds, and 1 Sell. That said, shares are priced at $463.61, and the average price target of $613.92 implies 32.5% upside potential over the next twelve months. (See SMCI stock forecast)

Dell Technologies

Next up is Dell Technologies, a well-known name from the personal computer world. Dell built its reputation on building PCs and laptops for the direct-to-customer market, and continues to hold a strong position in that market as a maker and supplier of PCs, laptops, monitors and gaming peripherals. The company has roots in the eighties; its modern incarnation dates back to 2016, when it acquired enterprise software and memory storage company EMC in a transaction valued at approximately $67 billion.

Since then, Dell has expanded its business footprint and now offers customers a range of hardware products to support networking and AI functions. These include high-performance server stacks and advanced memory storage, which are in high demand by AI developers, data centers and other technology companies that rely on high-performance computing architecture. Dell has applied its expertise in building computer systems – honed by its long experience in the personal computing segment – to advanced enterprise applications.

Looking specifically at the AI world, Dell can offer its customers solutions for desktop workstations, data centers, and even cloud-based computing. The company’s computing solutions and hardware can support generative AI applications including content creation, coding, personal digital assistants and design tools – the list is as long as the imagination of AI developers.

Dell’s latest financial report covered the second quarter of 2025, and the company beat expectations on both the top and bottom lines. Dell’s quarterly revenue rose more than 9% year over year to $25 billion, beating forecasts by $910 million. The company’s earnings, reported as non-GAAP earnings per share of $1.89, were 18 cents per share better than expected.

Prominent among Dell’s revenue drivers were the Infrastructure Solutions Group, which saw a 38% year-over-year increase to $11.6 billion, and the Networking segment, which rose 80% to $7.7 billion. Both figures were segment records for the company.

Contacting Vijay Rakesh again, we find the analyst bullish on Dell, noting that the company has built a solid AI hardware business without skimping on its existing retail PC business. Rakesh says of Dell: “We see DELL well positioned in the AI server race with a strong NVDA partnership and aggressively gaining market share with pricing, but still diversified into PCs, conventional servers, services and storage solutions. We see an Enterprise storage refresh and a potential Win11 refresh cycle for business PCs in 2025 as a tailwind, as with AI PCs, that could drive both consumer and enterprise upgrades.”

Looking ahead, the analyst outlines plenty of reasons to expect continued strong performance, writing: “We see potential for $9+ EPS for DELL in F26E (~$10+ EPS in F27/C2026) as it continues to gain market share in AI- servers. maintains a strong position in computer servers and sees PCs returning to growth after F24 saw weaker EPS, mainly due to a ~14% year-over-year revenue decline, offsetting stronger margins.”

According to Rakesh, Dell gets an Outperform (buy) rating, and he supplements that with a $135 price target, which indicates a 15% upside over one year.

Dell’s 17 recent analyst reviews include 14 for Buy and 3 for Hold, for a Strong Buy consensus rating. The shares are trading for $117.31 and their average price target of $144.63 suggests upside of 23% or more by this time next year. (To see DELL stock forecast)

Comparing the data for these stocks, it’s clear that for this top analyst, Dell Technologies is the superior AI hardware stock for investors to buy.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is for informational purposes only. It is very important to do your own analysis before making an investment.